In the first quarter of 2017, Consumer Enforcement Watch tracked 46 enforcement actions taken against consumer financial service providers. This represents a slight decrease from the 50 enforcement actions taken against consumer financial service providers in Q1 of 2016. 34 of the 2017 Q1 enforcement actions were settlements (with or without consent orders), while the remaining actions were court judgments, new actions, and new activity in ongoing enforcement actions.

var divElement = document.getElementById(‘viz1496927765448’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; vizElement.style.width=’654px’;vizElement.style.height=’929px’; var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

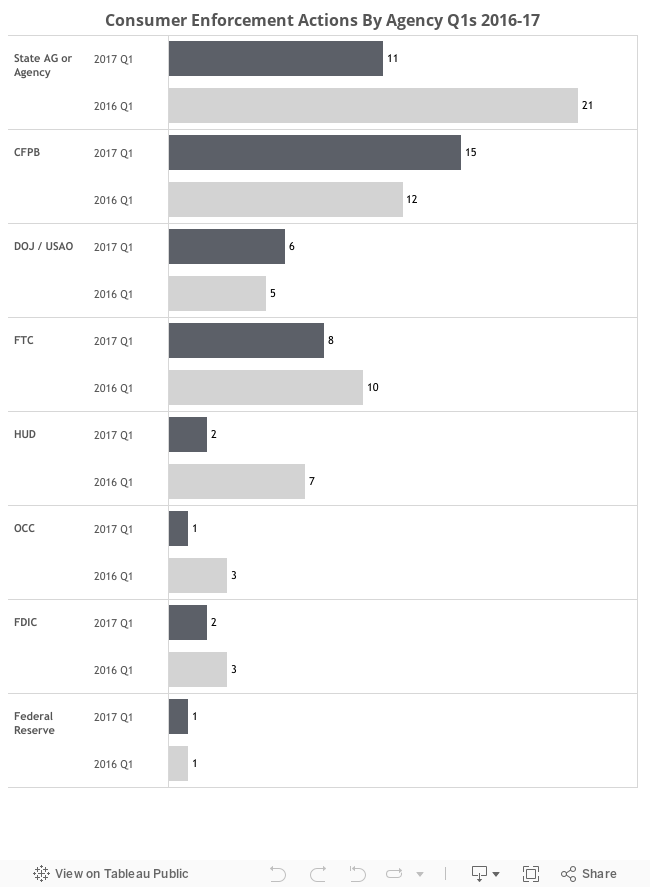

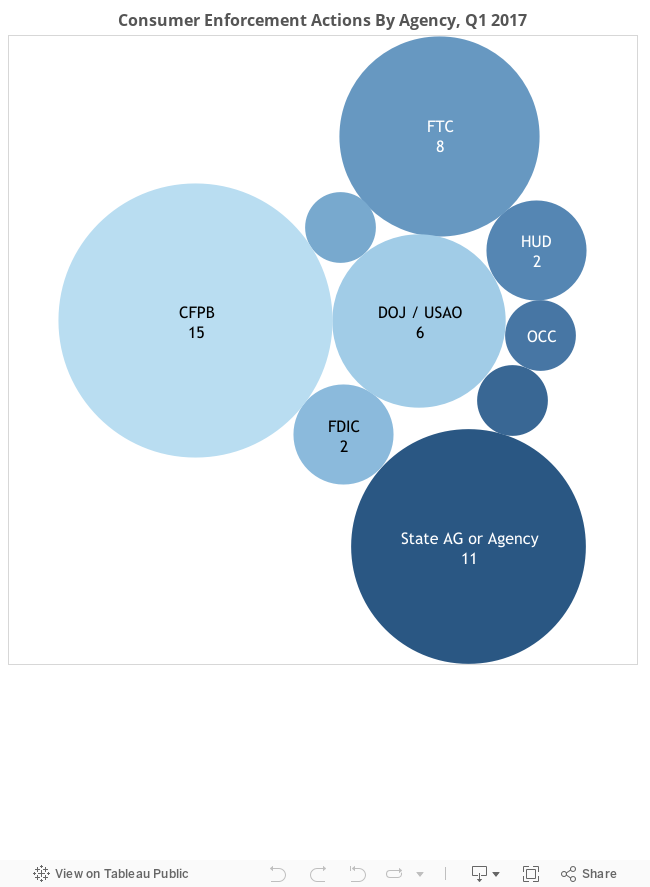

State enforcement actions continued to decline, consistent with the trend observed last year. In Q1 2016, state enforcement agencies were involved in 15 of the enforcement actions tracked, and 71 of the enforcement actions tracked for the year. In Q1 of 2017, state enforcement agencies were only involved in 11 actions. Similarly, the Department of Justice (DOJ) and the United States Attorney’s Office is on track for fewer actions in 2017; however, the change in administration could result in a slow start in 2017.

Conversely, in 2017, the Consumer Financial Protection Bureau (CFPB) is on pace to at least meet, if not surpass, the number of enforcement actions brought in 2016. Unlike the DOJ and U.S. Attorney’s Offices, the CFPB is not subject to an administration. CFPB’s increased activity may also be attributable to the increased pressure on and uncertainty facing the agency following the D.C. Circuit’s ruling in PHH v. CFPB, No. 15-1177 (D.C. Cir.), last fall. The D.C. Circuit reheard that case en banc on May 24, 2017. A decision is pending.

Although CFPB enforcement has increased over the past several quarters, state enforcement agencies have been bringing fewer enforcement actions. In Q3 of 2016, state enforcement agencies brought eight new enforcement actions. In this quarter, state enforcement agencies brought only one new enforcement action, and two joint enforcement actions with the CFPB. This quarter, the FTC, the CFPB, HUD, and the DOJ were jointly responsible for eight new enforcement actions.

var divElement = document.getElementById(‘viz1496927922296’); var vizElement = divElement.getElementsByTagName(‘object’)[0]; vizElement.style.width=’654px’;vizElement.style.height=’929px’; var scriptElement = document.createElement(‘script’); scriptElement.src = ‘https://public.tableau.com/javascripts/api/viz_v1.js’; vizElement.parentNode.insertBefore(scriptElement, vizElement);

The Consumer Financial Protection Act (CFPA) continues to be the statute most frequently at issue in Q1 actions, cited 12 times. The Federal Trade Commission Act (cited 9 times) was also frequently invoked. This quarter saw the first marketing service agreement enforcement action in years, as well as an increased focus on “rent-a-tribe” schemes, which the CFPB is currently challenging in the Ninth Circuit. CFEW continues to track this and other related actions and track in Q1 three alleged “rent-a-tribe” schemes that resulted in enforcement actions, which can be read here, here, and here.

Mortgages remained a primary enforcement target, with 13 mortgage-related enforcement actions in Q1. Although mortgages remain the most common enforcement target, we are now on pace for just 52 mortgage-related enforcement actions in 2017, representing a small increase from the 45 mortgage-related actions we tracked in 2016, and a slight decrease from the 68 actions we tracked in 2015.

The first quarter saw an increase in the amount of enforcement actions related to personal loans (5), and debt settlement (7). Enforcement related payday lending (4) and debt settlement (3) was similar to last quarter, while the number of credit reporting enforcement actions (2) and credit card enforcement actions (2) increased from the previous year.

Federal and state actions resulted in just over $667.1 million in civil penalties and settlement payments to the government this quarter. $65 million of this amount came from a penalty issued against a default management company, and another $35 million came from an action brought by the North Carolina Attorney General against three debt relief companies.

Enforcement agencies also collected approximately $508.6 million in consumer relief or restitution, which is significantly higher than the $31 million that Enforcement Watch tracked in Q2 of 2016, or $100 million in Q3 of 2016, but less than the $750 million tracked in Q1 of 2016. Of the $508.6 tracked this quarter, $225 million came from a consent order a mortgage servicer entered into with the California Department of Business Oversight.

Consumer Finance Enforcement Watch will continue to post quarterly and annually on trends in consumer finance enforcement activity. For specific questions regarding trends by enforcers, industry, or other data, please feel free to contact Kyle Tayman, Levi Swank, or Matt Riffee.